We are pleased to share some useful information on PIT for expatriates provided by our member, Domicile.

Understanding Personal Income Tax in Vietnam for Expatriates

In Vietnam, the tax system can be at times confusing and tedious, involving procedures and calculations that sometimes are complicated and hard to comprehend, mostly for expatriates, foreign individuals that have no technical knowledge on the Personal Income Tax rules and regulations applied to, salaries, wages and other sources.

What is Personal Income Tax?

While “Personal Income” refers to an individual’s total earnings from wages, investments, and other activities during a given period, the Personal Income Tax represents the amount of taxes an individual is required to pay into the Vietnamese state budget from salary deductions and other sources of income.

A few examples for sources of Personal Income which are subject to Personal Income Tax are: salaries or monthly incomes, inheritances, franchising income, transfer of real estate, capital transfers, capital investment, business activities, copyrights and prizes, with the note that the taxable income refers to the income generated in and out of Vietnam, regardless of where the income is paid.

Resident or Non-Resident?

Depending on the foreigner’s residency status, Personal Income Tax calculations can be substantially different, depending on the level income the individual earns.

Foreign individuals will be defined as “Tax Residents” where they meet ONE of the conditions below:

- Are present in Vietnam for a period of 183 days or more within either a calendar year or for 12 consecutive months, counting from the 1st arriving date, or

- Have a permanent residence in Vietnam, representing a registered residence which is recorded on a Temporary/Permanent Residency Card, or

- Have signed a rental contract for a period over 183 days.

If the above tests are not met, then an individual will be treated as Non-Tax Resident in Vietnam. However, care still needs to be taken as there are circumstances where an individual may still be deemed a tax resident in Vietnam if they cannot prove they are Tax Resident in another country.

Taxable Income

The notion of Taxable Income is essential in the calculation of the PIT for foreign individuals, regardless they are Tax Resident or Non-Tax Resident in Vietnam, and it is important to understand what this refers to.

For Tax Residents, Taxable Income is represented by all income which is generated world wide, regardless of where the income is paid or received. For a Non-Tax Resident, all income received for work undertaken in Vietnam, regardless where it is received. This means that if the foreign individual is engaged under a contract work in Vietnam but gets paid in an offshore account, these funds are generally liable to Personal Income Tax in Vietnam (other than where a specific Double Tax Agreement exemption applies). This is one of the common misunderstandings, and this is regularly debated in online media, among freelance consultants and expatriates involved project work, or digital nomads. This article is relevant to what the government is doing to actively pursue this issue in the tax system.

Personal Income Tax Calculation:

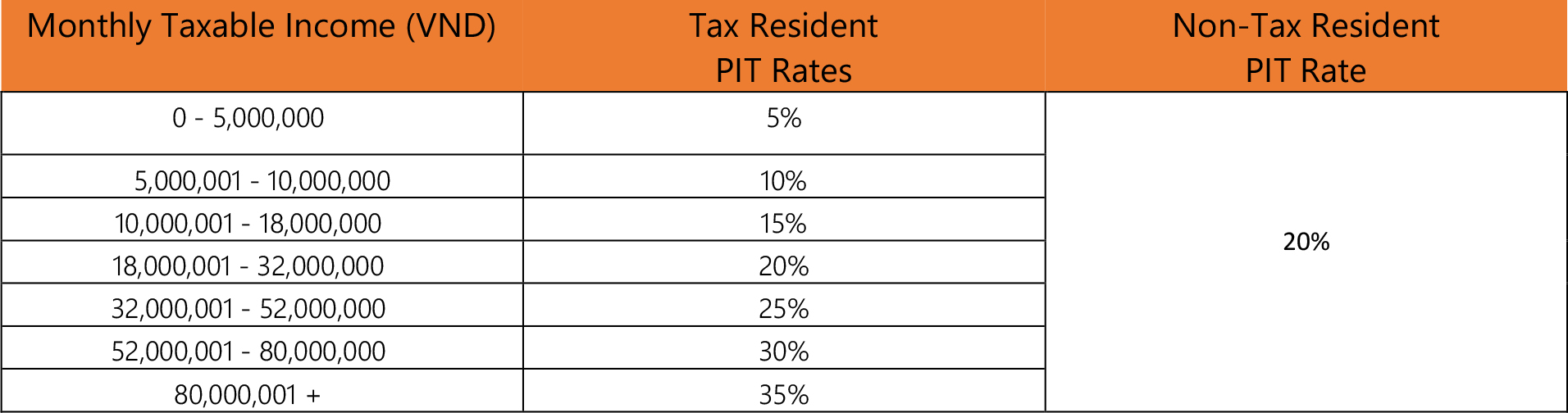

The Monthly Taxable Income generally represents the monthly salary or wage of the individual, and is taxed at a progressive rate from 5% to 35% for a Tax Resident, and a fixed 20% rate for a Non-Tax Resident, as in the chart below.

Notes:

-

a Personal deduction of VND9,000,000 is provided each month, which reduces the monthly taxable income accordingly.

-

additional dependent deductions are permitted, of VND3,600,000 per dependent per month, where they meet the requirement and are registered, further reducing monthly taxable income

-

Insurances withheld from employee gross salaries are deductible for PIT (ie, not subject to tax), and the employer contributions are not regarded as a taxable benefit for the employee.

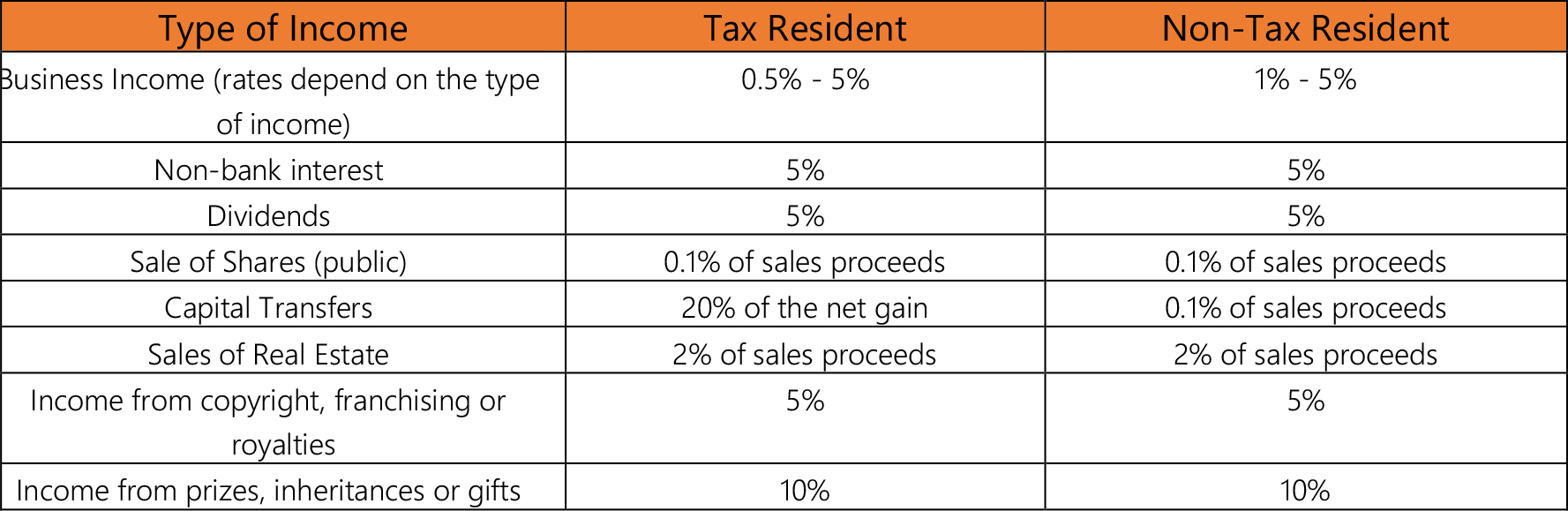

The Personal Tax Rates on Other Income range from 0.5% to 10% and are presented in the chart below:

Service Contracts

Individuals commonly enter into “Service Contracts” in Vietnam for short term activities, but as these are not Labour Contracts, PIT is not applied on the progressive scale. Instead, payments exceeding VND2,000,000 in a month will require 10% PIT (for Tax Residents) to be withheld and remitted by the paying entity (the company) as a pre-payment of PIT for the individual.

At the end of the year, this income will be included in the annualised/taxable income subject to PIT at progressive rates, and a credit will be given for the 10% already paid.

Any shortfall in taxes will need to be paid to the Tax Authorities upon finalisation.

PIT calculation in Vietnam can be completed by using the charts and thresholds presented above and a there are a few online calculators that can show an estimate of the amount that has to be paid.

Non-Taxable Benefits & Income

Although the definition of taxable income is broad, there are certain defined benefits that are excluded from taxation. These benefits include:

- Once per year round-trip airfares for expatriate employees returning home, or Vietnamese working abroad returning.

- School fees (excluding tertiary) for children of expatriate employees or for Vietnamese working abroad.

- Mid-shift meals (subject to a cap in provided in cash).

- One-off relocation costs for expatriates coming to Vietnam for employment, and for Vietnamese working abroad.

- Uniforms (subject to a cap if provided in cash).

- Benefits provided in kind on a collective basis (eg, memberships) where an individual is not identified as beneficiary.

- Allowances or benefits for weddings or funerals.

Additional Income that is not taxable includes:

- Interest earned on deposits with banks and credit institutions.

- Payments from life and non-life insurance policies.

- Retirement pensions paid from the Social Insurance Fund.

- Transfers of property between direct family members.

- Inheritances and gifts from direct family members.

- Monthly retirement pensions from voluntary insurance schemes

- Income from winnings at Casinos.

Tax Years and Finalisations

Foreign individuals are subject to a calendar year as their standard tax year. Employers are required to withhold PIT from employee salaries and remit monthly or quarterly (depending on the size of the employer).

Other taxes are generally required to be withheld at source (ie, dividends), or self declared on an events basis.

Within 90 days from the end of a tax year, individuals will need to determine whether they will need to undertake an annual tax finalisation.

If an individual only has income from a single employer during the year, then they can authorise their employer to finalise on their behalf. Non-residents don’t need to finalise for Personal Income Tax from Salaries and Wages.

If an individual wishes to claim a tax refund, a tax credit for future years, or has a tax liability to the tax authorities, then they must complete a tax finalisation within 90 days from the end of the tax year.

Individuals with simple tax matters, and who do not owe any taxes to the authorities, do not need to finalise. However, this may have an impact on future years if their tax affairs become complicated, therefore all taxpayers are encouraged to finalise their taxes each year.

Official Letters and Clarifications

Official Letters are releases showing the Tax Authorities’ interpretation and application of Vietnam’s Taxation Laws, providing guidance to taxpayers in Vietnam.

On 21 January 2019, HDT issued Official Letter 3228/CT-TTHT providing guidelines for PIT on foreign employees.

Foreign individuals who are appointed by an offshore parent company to work at a subsidiary in Vietnam for a long period, and are determined as a tax resident in Vietnam, will be subject to PIT in Vietnam on their global income.

The subsidiary is responsible for withholding and declaring PIT for domestic income paid to the foreign individual. For income received from the offshore parent company, the individual is required to self-declare on a quarterly basis following form 02/KK-TNCN issued in Circular 92/2015/TT-BTC.

Where the individual is determined as a tax resident, they are required to finalize their PIT. If the total income is only from the Vietnamese subsidiary, they are eligible to authorize the subsidiary to finalize PIT on their behalf. However, if they receive income from both the subsidiary and the parent company, they must self-finalise the PIT.

Double Taxation Agreements

These agreements take place to avoid having a situation where a tax payer will pay tax on the same income twice, one in Vietnam and once in his domicile country.

Tax relief in Vietnam under a DTA is not automatic. Foreign taxpayers are required to submit a notification application to the Vietnamese tax authorities 15 days prior to the tax payment deadline in order to seek to apply double taxation relief.

Applications can still be submitted in arrears up to 3 years from the tax payment due date, however implications may arise with late filed applications.

The DTAs also have the following purposes:

- Exemption or reduction of payable tax amounts in Vietnam for residents of the signatory country,

- Deduct the amount of tax paid by the Vietnamese Resident in the Contracting State from the amount payable in Vietnam.

- Supporting the signatory countries to prevent tax evasion on taxes on income and assets.

For further contact:

Vlad Savin, Business Development Executive, email: vlad.savin@domicilecs.com

Matthew Lourey, Managing Partner, email: matthew.lourey@domicilecs.com